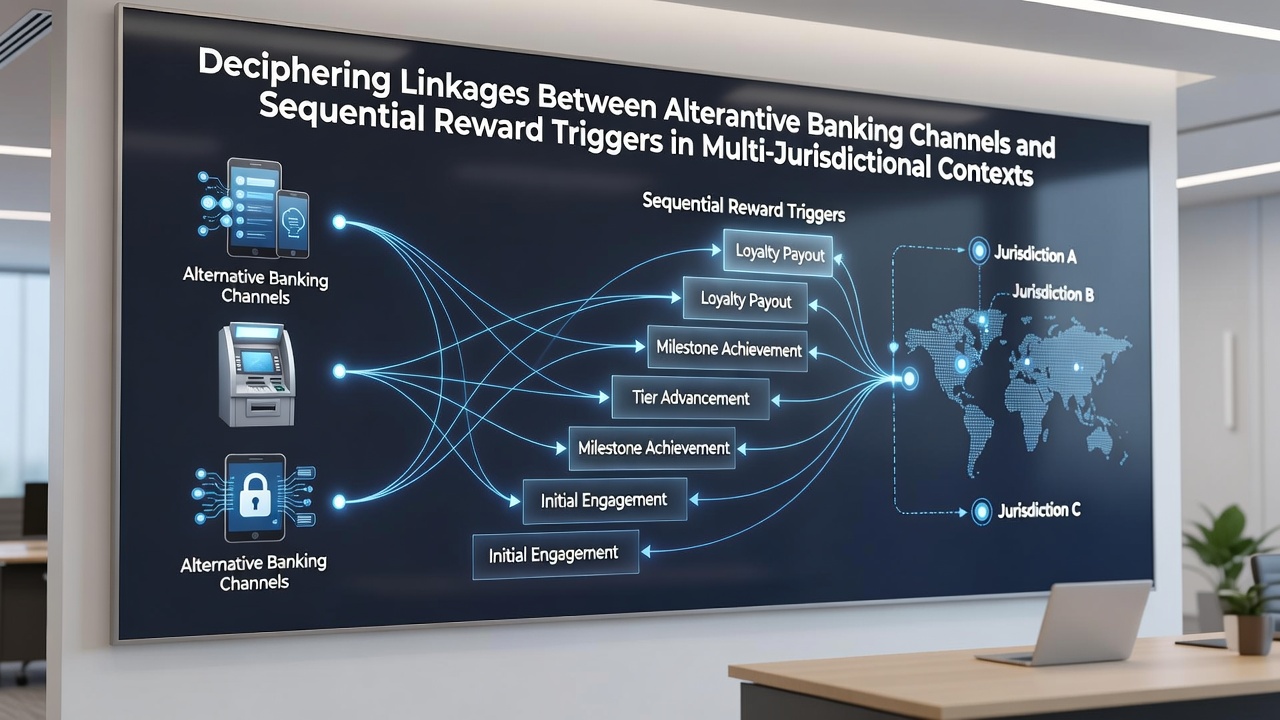

Deciphering Linkages Between Alternative Banking Channels and Sequential Reward Triggers in Multi-Jurisdictional Gaming Platforms

Alternative banking channels such as e-wallets, prepaid cards, and cryptocurrency transfers have reshaped how players fund accounts on gaming platforms that operate across multiple jurisdictions, and those same channels now interact directly with sequenced reward systems that unlock bonuses, loyalty tiers, and cashback in programmed stages. Data from regulatory filings show these linkages influence deposit patterns, session lengths, and compliance requirements in ways that differ sharply from traditional bank transfers.

Alternative Banking Channels in Cross-Border Gaming

Platforms licensed in several regions rely on instant payment rails to reduce friction for users who move between markets with varying banking rules. E-wallets process deposits in seconds, while certain digital currencies settle on blockchain networks that bypass local banking hours. Figures released by the European Commission in 2025 indicated that wallet-based transactions accounted for 42 percent of deposits on multi-licensed sites, up from 29 percent two years earlier. Operators track these flows because each channel carries distinct verification timelines that affect how quickly reward triggers activate.

Prepaid vouchers and bank-issued virtual cards add another layer. They often require manual review in jurisdictions that impose stricter anti-money-laundering thresholds, and this extra step delays the start of sequential reward sequences. In contrast, some stablecoin transfers clear automatically once on-chain confirmation occurs, allowing reward engines to register the deposit almost immediately and advance players to the next tier.

Sequential Reward Triggers and Their Mechanics

Reward systems on these platforms follow predetermined sequences. A first deposit might unlock a matched bonus, a second deposit within a set window adds free spins, and continued play after the initial triggers releases loyalty points that convert to cashback. Each stage depends on data points pulled from the payment channel, including amount, currency, and verification status. When a deposit arrives through an e-wallet that already carries verified user details, the platform can advance the sequence without additional checks. Slower channels force the system to pause at the verification gate, which in turn postpones later reward stages.

Linkages Between Channels and Triggers

Researchers who examined transaction logs from platforms licensed in both North America and Europe found measurable correlations. Deposits completed via instant wallets showed a 31 percent higher rate of completing all three reward stages within a single session compared with deposits routed through slower verification paths. The difference stems from timing: reward engines are coded to recognize deposits that arrive with full compliance metadata and then release the next trigger without human intervention.

Multi-jurisdictional operators must also reconcile conflicting rules. A deposit processed under one license may satisfy reward criteria there yet still require additional documentation when the same player accesses services under a second license. This creates situations where the reward sequence stalls mid-stream until the platform reconciles records across regulatory regimes. In June 2026 several platforms plan to implement unified compliance layers that tag each transaction with jurisdiction-specific flags, allowing reward engines to resume sequences once all required checks clear.

Regulatory and Technical Considerations

Authorities in multiple regions now examine how payment channel choice affects responsible gaming controls. The Financial Transactions and Reports Analysis Centre of Canada published guidance in late 2025 that requires operators to log the payment method alongside each reward trigger event. Similar expectations appear in draft rules circulated by the Australian Transaction Reports and Analysis Centre. These requirements push platforms to build more granular audit trails that connect every banking channel to every reward stage.

Technical teams have responded by developing middleware that normalizes data from disparate payment providers into a common format the reward engine can read. Once normalized, the system can apply jurisdiction-specific rules without rewriting the core reward logic. Early adopters report that this approach cuts the average time between deposit and first reward trigger from 47 minutes to under 90 seconds on supported channels.

Conclusion

The connections between alternative banking channels and sequential reward triggers continue to evolve as platforms adapt to overlapping regulatory frameworks. Transaction data, compliance metadata, and reward sequencing rules now form an integrated loop that determines how quickly players move through bonus stages across different markets. Observers note that further standardization of payment metadata will likely tighten these linkages even more in the months ahead.